- Banking

Why batch processed transaction enrichment is the silent enabler of modern payment fraud

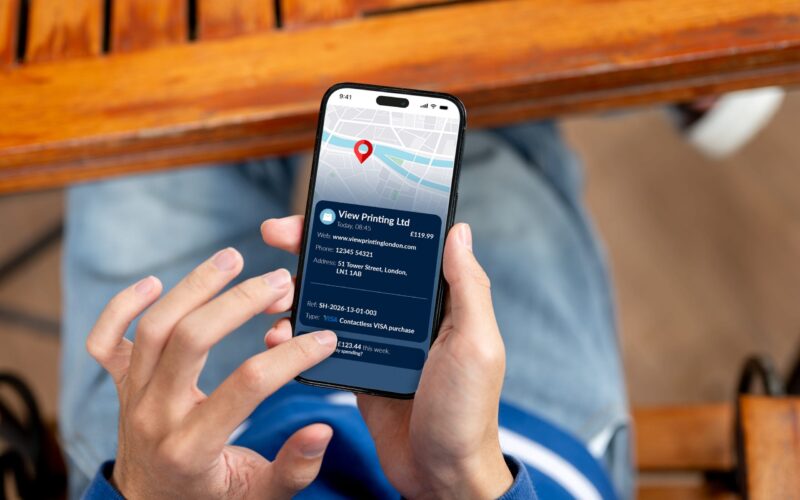

Modern fraud moves faster than batch process systems were designed to handle. Compare batch processing transaction enrichment versus real-time categorisation and enrichment to see where the opportunity lies for banks to reduce fraud.

Read more